|

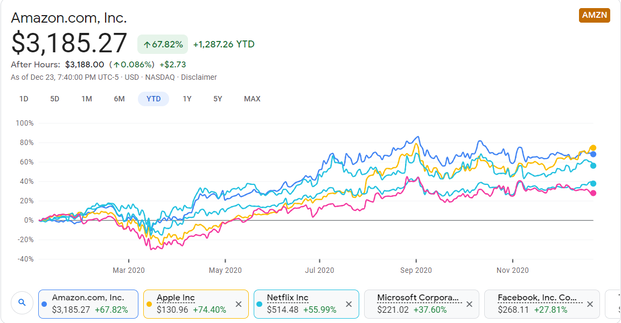

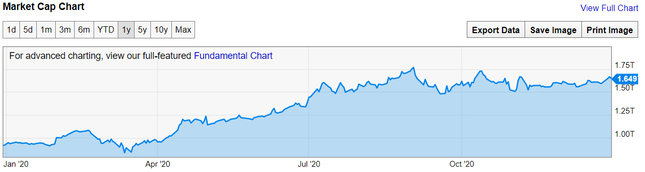

Perhaps the most fundamental problems with the recently-passed stimulus bill is not just the pettiness of the $600 one-time “relief” payment for Americans nor the enormity of the debt our government is currently stacking up for future generations to pay. Its biggest problem is that it does not adequately address the massive transfer of wealth that has taken place amidst almost a year of pandemic and lockdowns. And that’s not to mention the enormous budget deficit. Indeed, this looks bad…  St. Louis Federal Reserve Yet, even if the debt was not approaching $28 trillion and the deficit was not going to double revenue in 2020 and even if the stimulus payment was enough to keep afloat Americans who are living on the edge, the bill would still not suffice. The bill simply doesn’t address the massive transfer of wealth and consolidation of industry that has taken place in the last nine months. As The New York Times has noted, “More than 400,000 small businesses have already closed and millions more are at risk.” And some entire sectors have been simply devastated. As of September, a full 37 percent of small businesses in the leisure and hospitality industry were either temporarily or permanently closed. And this is unlikely to get much better with a new wave of lockdowns in many states. Many Americans are also hurting. While the economy is unlikely to collapse at this point and the unemployment rate has fallen back into the “bad, but not catastrophic” territory, many have had their savings wiped out. One survey back in September found that 14 percent of respondents had had their savings entirely depleted while another 11 percent had been forced to borrow money from a friend or family member. The new round of PPP in the stimulus bill is a good thing for hurting small businesses, although I doubt the $600 is going to help replenish Americans’ savings accounts. As of yet, there has not been the avalanche of evictions or foreclosures many have feared. Even still, various studies have alluded to the possibility of one in the near future and as many state’s lift eviction moratoriums in the next three to six months, what lies in store is yet unknown. If states and municipalities decide to leave those moratoriums in place indefinitely, many landlords will be pushed into foreclosure. Too many landlords (and homeowners too, of course) being foreclosed will cause banks to start failing. And at some point, if the government is going to bail all of these entities out with endless “stimulus,” the government will either run out willing lenders to borrow from or people’s faith in the dollar if they continue to print more. And if the world loses confidence in the dollar and the dollar proceeds to lose its status as the world’s reserve currency, it would trigger massive inflation that would wipe out whatever is left of America’s middle class. There’s another problem with simply trying to keep the economy afloat with monetary policy and unfunded stimulus, though. By doing everything in its power to keep interest rates low, the Fed raises demand for real estate and financial assets. More often than not, these assets are owned by the wealthy. And as economics 101 tells us, increased demand leads to an increase in price. Thus, much of what the federal government did to relieve the economy aided the wealthy by increasing the value of financial assets while at the same time, much of what they did to prevent Covid-19 from spreading aided big business because many small businesses were all but forced to close. And for this discussion, it doesn’t much matter whether you think the lockdowns were a sound policy based on science or a wild overreaction. You could believe absurdities like the entire virus was a hoax, Covid-19 is actually caused by 5G or, on the other side, that what we are going through far exceeds the Spanish Flu or even the Black Death. I believe the lockdowns were an overreaction but that’s beside the point. What matters here is that what has been done has been done. And as we have already seen, what was done made big business the big winner of the pandemic and subsequent lockdowns. You could argue (probably correctly) that big government is a winner too in terms of the powers it has accrued. But in purely financial terms, we have witnessed the largest transfer of wealth in the history of the modern world and it went to the top. Tech companies in particular were well-placed to benefit from the pandemic as doing things online is something close to your only shopping option when a stay-at-home order is in place. Here, for example are the stock performances of Amazon, Apple, Netflix, Microsoft and Facebook. Each is up between 20 and 60 percent in one single year.  Google Finance I’ll remind you that 400,000 small businesses have gone under. Amazon’s market cap (the total value of their outstanding shares) tells an even more startling story. In a single year it has almost doubled, from $915 billion to $1.65 trillion.  YCharts Do you know anyone who’s seen their net worth almost double in 2020? Indeed, we should probably ask whether the stock market should be hitting record highs in the middle of a recession at all.

Many have also made a big deal about how US billionaires have increased their wealth by over a trillion dollars since the beginning of the pandemic. This is a bit misleading since they use a starting point right after the stock market crashed in mid-March. Therefore, billionaires have made a trillion dollars after having lost a bunch of money. Despite that caveat however, billionaires are still up big in 2020 while most of the rest of the country is hurting. Unfortunately, as it turned out, we were certainly not “in this together.” Big business and billionaires have made fortunes. The government has gained all sorts of new powers. Some people who had government jobs or essential jobs or jobs that could be done from home have at least done OK. On the other hand, many small businesses or those with jobs that were “not essential” got wiped out. And that doesn’t even go into the deaths from Covid-19 and rapidly declining mental health across the country. It won’t require much convincing for socialists or left-leaning individuals to get onboard with a large redistributive Covid-19 tax on companies like Amazon and individuals like Jeff Bezos. But libertarian or market-oriented individuals will obviously be more hesitant. Indeed, I personally fall in the latter category. Usually arguments for low taxes note that we aren’t divvying up a static pie. Great entrepreneurs and business leaders (tend to) expand that pie, thereby it’s justifiable for them to keep a bigger share. While this is true in general, it doesn’t apply here. The pie isn’t bigger now than it was at the end of 2019. It’s smaller. A lot smaller. I would ask market-oriented individuals to consider the lockdowns to be an indirect but absolutely enormous form of corporate welfare. Again, we can argue all day as to whether the lockdowns were and are necessary or not, but the effect of those lockdowns clearly was and is corporate welfare. The great free market economist Ludwig von Mises once argued that one government intervention will almost inevitably require another to fix the problems caused by the first. Perhaps that is true. In this instance, it is absolutely true and if the words “require another” ever applied to a previous government intervention, it would be to the lockdowns. Perhaps you cannot “fix” the first intervention. But something needs to be done to right the ship, even if it inevitably won’t be perfect. Merely borrowing and printing more money is not going to undo or even mitigate the corporate welfare that was and is the lockdowns. Instead, a one-time Covid tax that scraped back a substantial share of the $735 billion in market cap Amazon has gained this year as well as much of the other gains made by Wall Street and various billionaires should be in order. It won’t be easy to execute and the government will likely have to buy stock with the tax revenue it accrues to prevent a market crash and then slowly sell off those shares over the next few years. And yes, I’m sure there will be plenty of pork and grift involved. But hasn’t there been plenty of that already? The risks of not doing it are much greater in my humble opinion. Right now the United States’ is at risk of turning into an outright plutocracy and plutocracies are notoriously unstable (and unpleasant). Furthermore, the revenue the Covid-19 tax brings in would be a huge boon for struggling families and small businesses (and perhaps the deficit too). Longer term solutions to the deficit, the growing displacement of workers by technology and increasing concentration of industry are necessary. But first and foremost, the glaring consolidation of wealth brought on by the lockdowns and pandemic need to be addressed. And that requires a targeted solution. And a large, one-time tax on the “winners” of the pandemic is the best solution I can see to achieve that.

Comments

|

Andrew Syrios"Every day is a new life to the wise man." Archives

August 2018

Blog Roll

Bigger Pockets REI Club Tim Ferris Joe Rogan Adam Carolla MAREI Worcester Investments Entrepreneur The Righteous Mind Star Slate Codex Mises Institute Tom Woods Consulting by RPM Swift Economics Categories

|

The Blog of Andrew Syrios

RSS Feed

RSS Feed